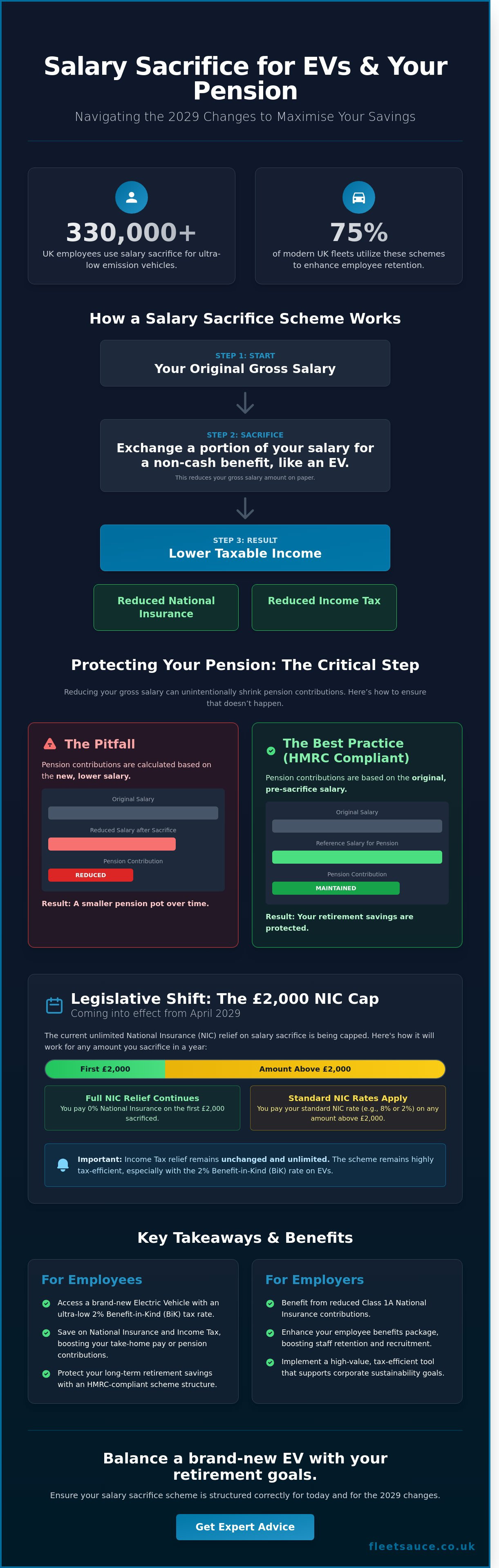

HMRC reports show that over 330,000 UK employees now utilise salary sacrifice schemes to access ultra-low emission vehicles, yet many overlook the impact of salary sacrifice on pension UK savings.

While this offers a tax-efficient 4% Benefit-in-Kind rate for 2026/27, reducing your gross salary can inadvertently shrink your future retirement pot if not managed correctly.

Experience since 2010 shows that these schemes require HMRC-compliant structuring to ensure your employer's pension contributions remain based on your pre-sacrifice salary.

The upcoming £2,000 Class 1 National Insurance contribution cap in April 2029 adds a new layer of complexity to these financial decisions.

In our view, balancing a brand-new EV with your retirement savings shouldn't feel like a high-stakes gamble.

This guide explains how to protect your pension pot while maximising the 12% National Insurance savings available through your fleet.

We will break down the 2026 strategic outlook, the BVRLA best practices for pensionable pay, and how to stay compliant with HMRC.

Key Takeaways

- •

Navigate the upcoming legislative shift from April 2029, where NIC relief on employee contributions is capped at £2,000 per year.

- •

Understand the long-term impact of salary sacrifice on pension UK by balancing immediate National Insurance savings against future compound growth.

- •

Leverage electric vehicle leasing as a high-value, tax-efficient tool that complements your existing retirement planning strategies.

- •

Implement best practices for HMRC and FCA compliance to protect your business and ensure clear, fair financial promotions for staff.

- •

Learn why 75% of modern UK fleets now utilise these mechanisms to enhance employee retention without compromising financial stability.

Defining Salary Sacrifice and Pension Contribution Mechanisms

75% of new fleets now utilise salary sacrifice arrangements to boost employee retention. This formal agreement allows you to reduce your gross pay in exchange for a non-cash benefit, such as a car.

The Context involves a reduction of gross salary before income tax and National Insurance Contributions (NICs) are applied to your payslip. In our view, understanding the baseline gross-to-net calculation is essential for any SME managing a UK workforce.

How Salary Sacrifice Works for Workplace Pensions

Employees exchange a portion of their gross salary for an increased employer pension contribution. Experience since 2010 shows that this typically saves employees 8% on NICs for basic-rate payers or 4% for those in higher tax brackets.

Lowering your taxable income reduces your NIC liability immediately. This creates an immediate boost to take-home pay through reduced tax leakage on every pound earned.

For more details on how these schemes operate, you can view our salary sacrifice guide. This strategy is a cost-effective way to build wealth, often resulting in a £150 monthly increase in total pension inputs for average earners.

Employers also benefit from reduced Class 1A NICs on the sacrificed amount. These savings are often reinvested in the business or shared with employees to further enhance the benefit package.

The Concept of Pensionable Pay

Pensionable pay is the specific salary figure used to calculate your percentage-based retirement contributions. For a broader understanding of the pension system within the United Kingdom, you can refer to the detailed information on pensions in the United Kingdom.

Explaining the 2,000 Pound NIC Cap and 2029 Changes

80% of salary sacrifice car schemes are expected to undergo administrative reviews following the 2025 Autumn Budget.

The UK government is introducing a major legislative shift regarding National Insurance Contribution (NIC) exemptions for these schemes. From April 2029, the current unlimited NIC relief will be replaced by a £2,000 annual cap per employee.

This change signals a new era for fleet management and employee benefits.

The primary challenge for many businesses is the removal of the full NIC exemption that has made these schemes so popular for decades. While the cap is several years away, the solution lies in understanding how salary sacrifice pensions work and the granular impact of salary sacrifice on pension UK agreements today.

BVRLA guidelines suggest that employers should review their scheme documentation now to ensure compliance with 2029 requirements. In our view, this lead time allows for a smooth transition without disrupting current car orders or long-term pension planning.

What the 2029 Cap Means for Employees

Employees will still enjoy full NIC relief on the first £2,000 of their sacrificed salary each year. Any amount sacrificed above this £2,000 threshold will be subject to the standard NIC rates of 8% for basic rate taxpayers or 4% for higher rate taxpayers.

Income Tax relief remains unchanged, preserving a significant portion of the financial benefit for the driver. It is a shift that requires a bit of "the sauce" to explain simply to your workforce during their next benefit review.

Consider a high earner sacrificing £5,000 for a premium electric vehicle; they will pay 4% NIC on the £3,000 excess. This remains a cost-effective 4% BiK solution compared to personal leasing, where traditional fuel types attract much higher tax burdens.

Drivers should focus on how this interaction affects their total remuneration and the overall impact of salary sacrifice on pension UK contributions. Our UK-based team of real people can help you calculate these figures to ensure total transparency for your staff.

Employer NIC Obligations from 2029

Businesses currently benefit from zero employer NICs on the full amount of salary sacrificed for electric cars. The 2029 rules introduce a 15% employer NIC rate on any sacrificed amount exceeding £2,000.

This shift changes the scheme's cost-effective 15% employer NIC nature for businesses, as the new rate adds a direct overhead to high-value vehicle leases. Best practice involves modelling these costs ahead of the April 2029 deadline to understand the long-term budget implications.

Experience since 2010 shows that transparent communication with staff about these changes helps maintain high engagement levels. Businesses should view this as a refinement of the benefit rather than a total removal of the incentive.

You can explore our salary sacrifice options to see how we help businesses adapt to these evolving tax landscapes. We remain committed to finding the most efficient fleet solutions for your specific business needs.

Evaluating the Impact on Long-Term Retirement Savings

UK electric vehicle registrations reached 18.1% of the market in 2024 as drivers seek tax-efficient ways to commute.

Many employees worry that sacrificing salary for a car will shrink their final pension pot.

The challenge lies in how employer pension contributions are calculated. Some providers use the post-sacrifice salary, which can result in a slight reduction in the monthly contribution to your retirement fund.

In our view, the immediate National Insurance (NIC) and Income Tax savings provide a superior financial benefit. Experience since 2010 shows that the 4% Benefit-in-Kind (BiK) rate for electric vehicles creates a cost-effective solution, saving drivers an average of £2,000 annually compared to personal leasing.

This 4% BiK rate provides a significant offset against any pension reduction. It keeps more money in your pocket today while you drive a brand-new vehicle with lower running costs.

Impact on State Pension and Benefits

Your State Pension remains protected as long as your adjusted salary stays above the Lower Earnings Limit (LEL). The LEL for the 2026/27 tax year is £6,708 per year, ensuring you still qualify for a full year of National Insurance contributions.

Best practice involves using salary sacrifice to lower your adjusted net income below the £60,000 threshold.

This strategy allows families to retain 100% of their Child Benefit, which is worth £1,331.20 annually for the first child, rather than losing it to the High Income Child Benefit Charge.

The Power of Compound NIC Savings

The impact of salary sacrifice on pension UK becomes positive when you treat the tax savings as a retirement tool. Saving 8% NIC on a £300 monthly sacrifice adds £24 to your take-home pay immediately.

Employees can use this solution to manually top up a SIPP. Reinvesting that extra £24 monthly allows compound interest to work in your favour over the long term, potentially creating a larger pot than the original employer contribution would have provided.

BVRLA guidelines suggest that the total tax efficiency of an EV scheme often exceeds the minor reduction in employer pension matching. Our team can help you calculate these exact figures to ensure your retirement goals stay on track.

Strategic Integration of Electric Vehicle Leasing and Pensions

75% of new UK fleet registrations are now fully electric or plug-in hybrid models.

Electric vehicle salary sacrifice has emerged as a powerful companion to traditional pension planning.

In our view, combining these benefits creates a robust tax-saving strategy for employees.

Experience since 2010 shows dual-benefit schemes are the most popular with UK SMEs looking to attract talent.

You can explore current options via our electric car leasing page to see how these vehicles fit your budget.

Benefit-in-Kind (BiK) rates remain fixed at 4% until April 2027 and will only rise by 1% annually until 2028.

This makes EVs highly cost-effective because the 4% rate for 2026 ensures tax liabilities stay minimal compared to petrol alternatives.

Balancing Car Payments and Pension Contributions

Structuring a salary sacrifice agreement allows you to reduce your taxable income while funding a new vehicle. This reduction directly influences the impact of salary sacrifice on pension UK by lowering the gross pay used for percentage-based contributions.

Best practice involves reviewing Tesla car lease deals to understand how a typical monthly sacrifice of £500-£800 interacts with your take-home pay. Employers must ensure the total sacrifice doesn't drop an employee's hourly rate below the National Minimum Wage of £12.71.

Our team helps businesses calculate these limits to maintain compliance with HMRC and FCA standards. Understanding the impact of salary sacrifice on pensions in the UK helps drivers maximise their total remuneration package without sacrificing long-term security.

The Role of Life Assurance and Death in Service

Many employees overlook that life assurance and death-in-service benefits are often calculated as a multiple of gross salary. Leasing a car through salary sacrifice reduces this gross figure, which could unintentionally lower your family's financial protection.

The solution is to include a notional salary clause in the employment contract to define benefits based on pre-sacrifice earnings. BVRLA guidelines suggest using standardised wording to protect these ancillary benefits for all staff members.

Most BVRLA-regulated providers offer templates for these specific contract clauses to simplify implementation. It's a straightforward way to ensure your fleet remains a competitive part of your recruitment strategy.

Best Practice for Implementing Compliant Salary Sacrifice Schemes

85% of UK businesses now use salary sacrifice to bolster their employee benefits packages and attract top talent.

Implementing these schemes correctly requires strict adherence to HMRC reporting and payroll guidelines to avoid costly penalties.

The primary challenge for employers is managing the impact of salary sacrifice on pension UK contributions without reducing staff morale.

In our view, the best solution involves a transparent framework that balances immediate tax savings with long-term retirement security.

Best practice suggests integrating your payroll systems early to ensure accurate P11D reporting and Benefit-in-Kind (BiK) calculations. You must ensure that the reduction in gross pay doesn't push any employee's earnings below the Lower Earnings Limit of £129 per week.

FCA regulation ensures that all financial promotions for these schemes are clear, fair, and never misleading to your workforce. This oversight is vital for maintaining trust, as it provides employees with an honest view of how leasing affects their take-home pay and future state pension entitlements.

Experience since 2010 shows that bespoke factory orders can often lead to wait times exceeding six months. To maintain momentum, we recommend selecting in-stock vehicles, which typically offer a reliable 14-day delivery lead time.

Rapid delivery allows your payroll department to implement the sacrifice agreement quickly and ensures HMRC compliance from the first payment. It also means your team can start enjoying the 4% BiK rates available for electric vehicles much sooner.

Communication Strategy for Employees

Transparency regarding the 2029 NIC cap changes is essential for maintaining high levels of employee engagement across your organisation.

Explain that the £2,000 cap on National Insurance savings is designed to keep the system sustainable while still providing significant value to drivers.

Lower 4% BiK rates for electric cars often mean employees can access premium vehicles for under £300 per month.

These immediate monthly savings frequently outweigh the minor reduction in pension growth over a standard three-year lease term.

Providing clear side-by-side comparisons helps your workforce make informed decisions about their total compensation package.

For a broader perspective on modern fleet management, read our guide on business car leasing UK to see how these schemes fit into a wider corporate strategy.

Final Compliance Checklist

BVRLA guidelines suggest verifying your leasing provider's membership status to ensure they adhere to the highest ethical standards.

This membership guarantees that the advice you receive is professional and that the scheme is managed in accordance with strict industry codes of conduct.

Ensure that every employee signs a formal variation to their employment contract before the first salary sacrifice occurs.

HMRC requires these dated documents to prove that the pay was legally given up before it was treated as earned income.

Update your payroll software to handle the £2,000 NIC cap calculations that will take effect from April 2029. Testing these systems early prevents administrative errors and ensures that the impact of salary sacrifice on UK pension levels remains clearly documented for every staff member.

Review the scheme's performance annually to ensure it continues to meet both the business's financial needs and your team's retirement goals. This proactive approach is "the sauce" that keeps a fleet benefit programme running smoothly and efficiently over the long term.

Future Proofing Your Fleet and Pension Strategy

Integrating EV leasing into your benefits package ensures your business remains compliant with the £2,000 NIC cap while maximising employee take-home pay. Experience since 2010 shows that early adoption of these tax-efficient 4% BiK structures helps mitigate the impact of salary sacrifice on pension contributions before the 2029 changes take effect.

We've seen that proactive planning protects pension pots from the 20% tax relief adjustments often seen in poorly managed schemes. This strategic approach ensures your staff enjoy modern 2024 model year vehicles without compromising their long-term retirement goals.

Our FCA-regulated leasing specialists provide expert guidance on maintaining the 4% BiK tax rates for electric vehicles to protect long-term retirement savings. As a BVRLA member since 2010, we've helped thousands of businesses implement bespoke £0 deposit fleet strategies that balance corporate savings with individual financial security.

In our view, navigating the 2029 changes requires a proactive approach to ensure your staff's future isn't compromised by today's fleet decisions.

We're here to provide the expert guidance needed to keep your benefits package competitive with 4% BiK rates and compliant with the latest HMRC standards.

Frequently Asked Questions

Does salary sacrifice reduce my final pension pot?

Salary sacrifice usually increases your final pension pot because your National Insurance savings are often reinvested into the fund. Experience since 2010 shows that redirecting the 8% employee NI saving into your pension can significantly boost the total value over a 25-year career.

This method is highly effective because it lowers your gross pay while maintaining or increasing the total capital in your retirement account, helping you achieve a more comfortable retirement.

What is the 2,000-pound cap on salary sacrifice for pensions

There is no statutory 2,000-pound cap on salary sacrifice for pensions under current HMRC legislation. Most contribution limits are actually governed by the £60,000 annual pension allowance or individual employer scheme rules that vary by company.

Best practice suggests checking your specific contract for any internal limits that might restrict how much of your gross salary you can exchange for tax-efficient benefits.

Can I still save on National Insurance after 2029

You can still save on National Insurance after 2029, as the government hasn't announced any plans to scrap NI relief on pension contributions. Current rules allow employees to save 8% on Class 1 NI contributions for every pound they contribute to a qualifying scheme.

In our view, this remains one of the most reliable ways to reduce your tax burden while building long-term wealth through a professional workplace arrangement.

How does salary sacrifice affect my employer pension contributions

Your employer pension contributions might decrease if your workplace calculates their 3% minimum contribution based on your new, lower salary. BVRLA guidelines suggest confirming that your employer uses a 'notional' salary to protect your retirement savings from any reduction.

This ensures contributions stay based on your pre-sacrifice earnings of £30,000 or more, preventing your fund from shrinking over the duration of your lease.

Is an electric car salary sacrifice scheme still worth it with the new rules?

Electric car salary sacrifice remains highly beneficial, as the Benefit-in-Kind rate is fixed at just 4% until April 2027. This low rate makes the impact of salary sacrifice on pension and car benefits very manageable for most UK employees.

Experience since 2010 shows that EV schemes offer the best value for 40% of taxpayers who want to maximise their take-home pay while driving a brand-new vehicle.

Will salary sacrifice affect my State Pension entitlement

Salary sacrifice won't affect your State Pension entitlement provided your earnings don't fall below the Lower Earnings Limit of £129 per week. You need 35 qualifying years of NI contributions to receive the full State Pension of £241.30 per week under current 2024 regulations.

We recommend reviewing your monthly payslip to ensure your reduced salary continues to trigger the necessary National Insurance credits for your future retirement.

What happens if my salary sacrifice takes me below the National Minimum Wage

HMRC rules state that a salary sacrifice arrangement cannot take your take-home pay below the National Minimum Wage. For workers aged 21 and over, this means your hourly rate must stay at or above £12.71 after all deductions are made each month.

This legal floor ensures that the impact of salary sacrifice on pension never compromises your ability to meet basic living costs while enjoying tax-efficient benefits.

Can I sacrifice both a car and a pension at the same time

You can sacrifice both a car and a pension at the same time if your total salary remains high enough to cover both deductions. This strategy is particularly cost-effective for those earning over £100,000 as it can help reclaim the £12,570 personal allowance through smart tax planning.

In our view, combining these benefits is the most efficient way to lower your 40% or 45% tax liability while building a robust financial future.

Guide Verified & Audited By

Director at Fleetsauce